Every year since 1976, Warren Buffett (aka The Oracle of Omaha), chairman and CEO of Berkshire Hathaway based in Omaha, NE, has been penning an annual letter to shareholders describing his approach to buying stocks using good humor, down to earth language, jokes and useful anecdotes. Topics covered have included investment philosophy, portfolio management, corporate governance, diversification, and the limitations of Generally Accepted Accounting Principles (GAAP). The letters also discuss employing incremental capital, selecting business managers, and compensation policies. Also included are share repurchases, stock options, mergers and acquisitions, and the economics of the insurance industry.

The Beginnings

At the beginning of each year, anticipation grows as investors speculate on what Buffett will opine on in his annual letter. There is a lot of content in his letters to unpack in a brief commentary so I will focus on his investment philosophies. Here is a quick history of how Berkshire Hathaway came about. In 1964, Buffett purchased a controlling interest in Berkshire Hathaway which was then a company in the declining textile industry. By 1967, he began to invest in the insurance industry among other industries. Today, GEICO, which he bought in the late 1970’s, is the core of Berkshire’s insurance operations. Well run Insurance operations generate enormous amounts of capital which Berkshire has used ever since to make new investments in a variety of industries, including aviation with FlightSafety International which was acquired in 1996 and NetJets in 1998.

Value-Based Investing

The key quote in this year’s letter is clear and succinct: “Despite some severe interruptions, our country’s economic progress has been breathtaking. Our unwavering conclusion: Never bet against America.”

Touched on annually in his letter to shareholders, Buffet is never shy to outline his investment and diversification philosophies. It is no secret Buffet takes a long-term, value-oriented approach to investing, which has proved to stand the test of time and withstand market turmoil. For those of you who do not know the value investing philosophy, it is based on the idea of business fundamentals – such as earnings growth, dividends, cash flow, book value – rather than other influences on stock prices. Demonstrated in his letter, Buffet displays his commitment to value-oriented companies by outlining Berkshire’s sizable positions in Chevron, Verizon, and Coca-Cola. All companies who pay strong dividends, have stable earnings and all of which are held within our portfolios at MCIA. Today, the structure of our portfolio is heavily weighted in value-based companies that are stable, safe, and pay strong dividends.

The Opportunity

Given Buffett’s value investing strategy, it is not surprising that Berkshire substantially underperformed the market since the beginning of 2019. The fund has historically been very light on emerging technology driven companies maintaining the philosophy that slow and steady wins the race in the long run.

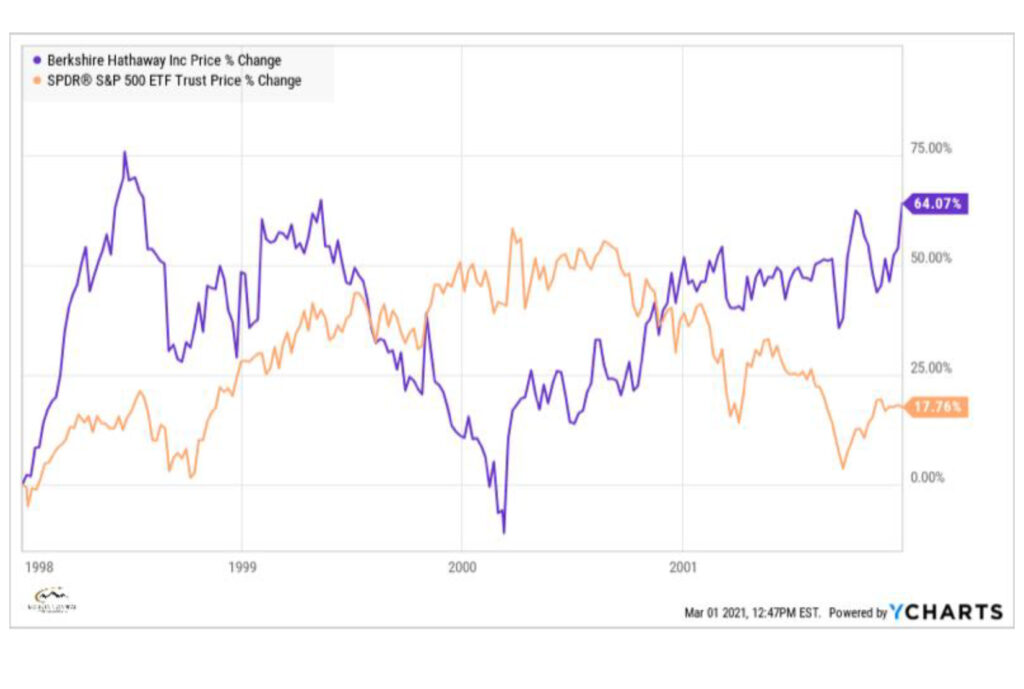

To illustrate the opportunity, the chart below compares market performance of the S&P 500 vs. Berkshire Hathaway during the Dot-Com bubble period between 1999 up to when it burst in late 2002. I was in the institutional equities business during that time and was amazed at the blind stampede into any company that claimed to be internet related, many with “.com” in their name. It makes sense that as the bubble reached its peak in March 2000, Berkshire substantially underperformed. But it is clear that following the collapse, Buffett’s long-term investing philosophy came back strong in the following 2 years.

Now looking at current performance in the chart below, Berkshire has underperformed noticeably as the flurry of new companies in information and technology, “green energy” and the “gig economy” have come public, most of which are yet to be profitable, have relatively low revenues to their size, and are projecting losses for years to come. The valuations on many of these companies defy logic on many levels. While historical performance is no guarantee of future performance, I am confident that what played out following the dot.com collapse will ultimately repeat itself over the next few years. That is the opportunity in front of us.

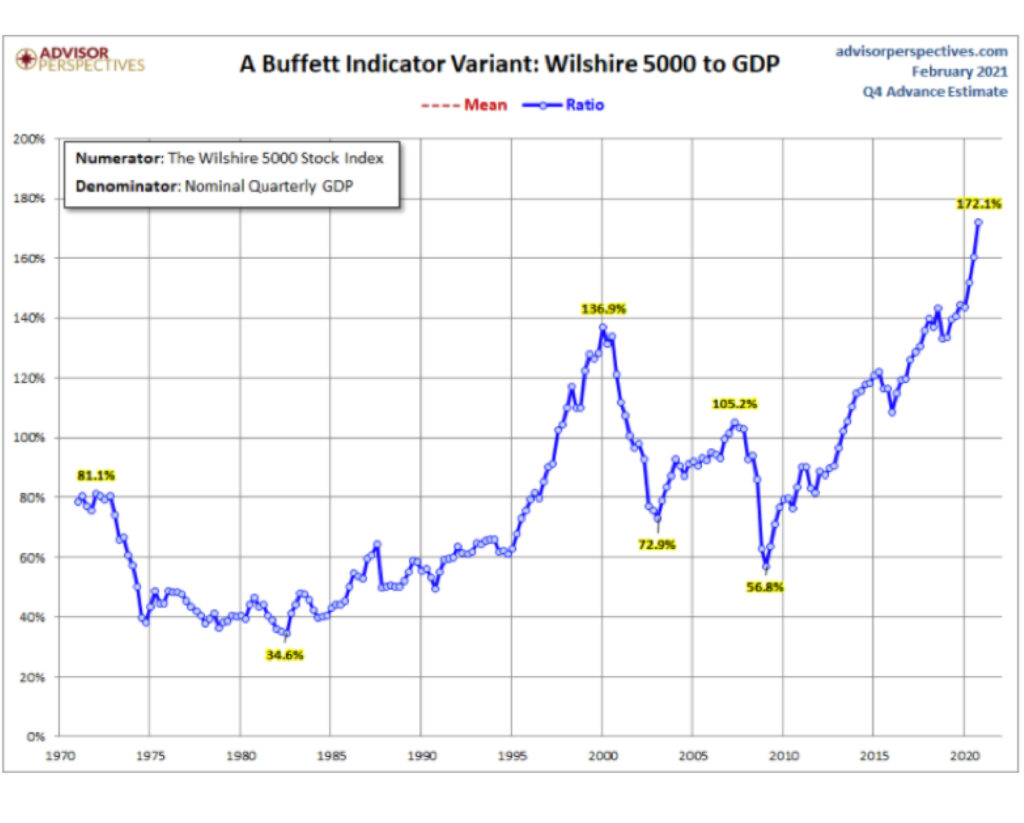

This may remind you of a point I made in previous notes highlighting the Buffett Indicator which is the ratio of the capitalization of the broad market to the current level of GDP. The sharp rise in market value over the last few years has pushed the ratio to record levels. It was high when I last mentioned it and is even higher today. An updated Buffett Indicator chart is included below. The point of reference I focus on is how the current ratio is 25% higher (136.9% vs 172.1%) than it was at the height of the dot.com craze. If there is one fundamental way to gauge valuation of the market, it is to compare it to the value of the economy.

Wrapping Up

As we have been communicating to everyone for several months now, we are firm believers that the shift to more value-oriented sectors of the market is beginning. These shifts take time to play out and, as expected, volatility comes with it as we saw this past month when the price momentum of so many very large, young, popular companies slowed.

More stimulus is coming, and vaccination rates are climbing fast, which is setting up for potentially explosive economic growth in the second half of this year. Barring another wave of COVID infections, the opening of the US and global economies will continue. All of that points to a broadening of market performance in under-owned industrial and consumer sectors of the economy. And on that note, all of us at MCIA wish everyone good health and prosperity in the weeks and months to come. As always, we are here to serve you so please never hesitate to call anyone on the team if there is anything you need or if you simply want to catch up.