As 2024 begins to unfold, housing market trends are one of the most talked about aspects of the year ahead. There are a number of factors at play when it comes to trying to understand how we got here and what we can expect in 2024. It’s obvious the surge in home values began as the pandemic took hold and interest rates plummeted. It would make sense that as interest rates began their sharp rise in March of 2022, increases in home values would slow which they did. That said, the second half of 2023 surprised economists with home value trends picking up again.

Below I will explore the following trends:

- Mortgage Rates

- Home Value Appreciation

- Rental Values

Mortgage Rate Trends

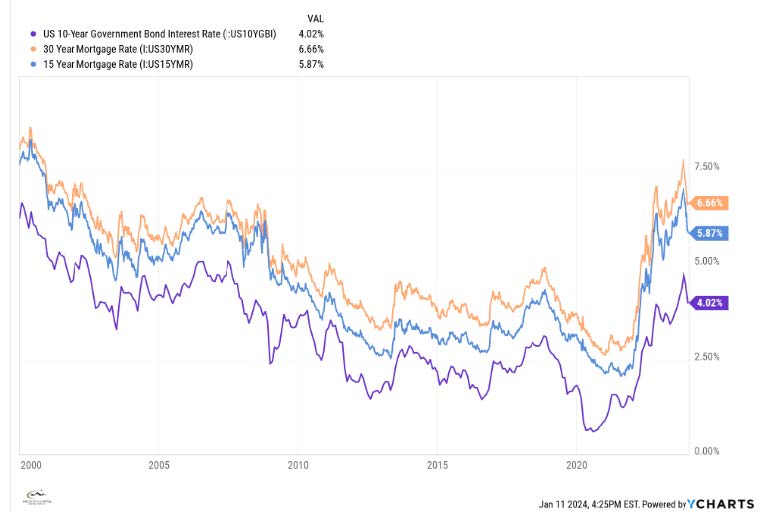

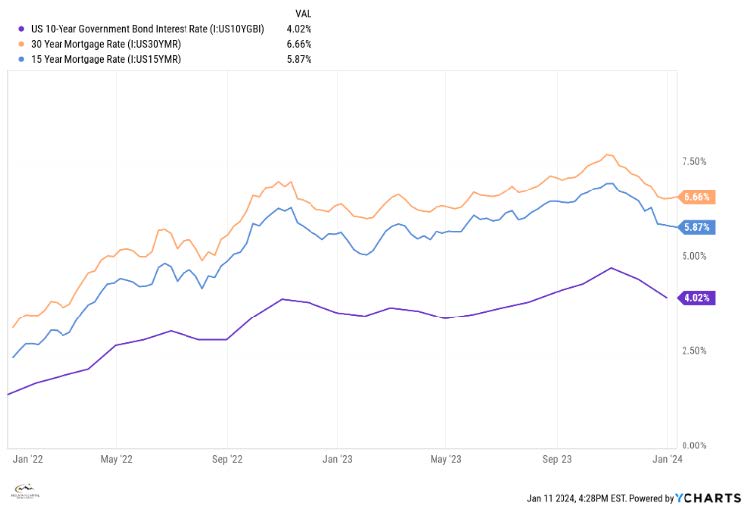

Below are two charts showing the history of 30-year and 15-year fixed mortgage rates going back to year 2000 and again going back to the start of 2022 when the Fed began to raise the Federal Funds Rate. Just in the past few months have we seen mortgage rates slowly decline in anticipation of rate cuts. I added to the charts the yield on the 10-year US Government bond to illustrate how it is essentially a proxy for mortgage rates given the fairly tight correlation. The outlook for interest rates in 2024 is mixed in that most analysts feel the drop in rates over the past view months has effectively priced in the odds of the beginning of rate cuts anticipated by this spring. That said, rates could bounce around the current levels and maybe even tick up a bit before the Fed plans for the year become clearer.

Home Valuation Trends

The housing market remained frozen in 2023 due to lack of supply and high mortgage rates adding to affordability pressures. The lack of housing supply was partly driven by the rate lock-in effect. The Federal Home Loan Mortgage Corporation, commonly known as FreddieMac, uses the term “mortgage rate lock-in effect” to refer to the impact that ownership of a mortgage on a favorable term compared to current market interest rates has on a homeowner’s incentive to sell their house. In 2020 and 2021, mortgage rates fell significantly hitting a historic low of 2.65% in January 2021 prompting many existing homeowners to refinance into these lower rates. Nearly 6 out of 10 borrowers now have a mortgage rate below 4%. Since then, mortgage rates have increased from the historical lows to 23-year highs. While rates have come down since the end of October, they remain well above 4%. With higher rates, the incentive for existing homeowners to list their property and move to a new house has greatly diminished leaving them rate locked.

Early in 2023, it appeared we were finally entering the “calm after the storm” phase for house prices where homebuyers would finally see some relief from the post-pandemic demand shocks that resulted in near-20% year-over-year house price appreciation over the previous two years. The latter half of 2022 saw a sharp slowdown in house price growth that carried into the first couple of months in 2023. Specifically, the Freddie Mac House Price Index (FMHPI) annual rate of growth decelerated from 18.8% in February 2022 to 0.9% in April 2023. The slowdown in home price growth was the direct result of the rapid deterioration in affordability that began in 2022 and continued into 2023.

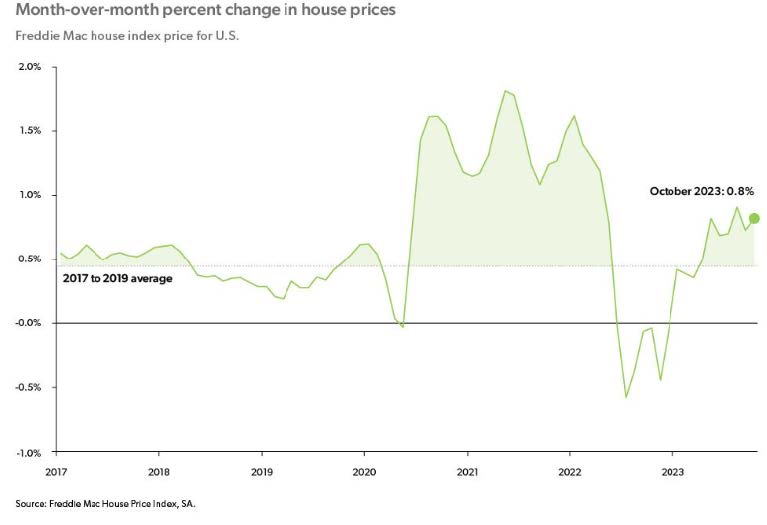

However, market forces prevailed in the second half of 2023 and home prices began to re-accelerate. Part of the reason prices have climbed was because of stubbornly low inventory. People that could absorb higher mortgage rates or who were paying cash competed for the few homes available. Combined with the fear from many buyers that if they don’t buy now, interest rates could increase even more so prices moved higher. The chart below shows that house prices grew at a monthly rate of 0.8% in October 2023, which translates to an annualized rate of more than 10%. Additionally, since May 2023, month-over-month house price growth averaged 0.8%, which is above the 2017 to 2019 pre-pandemic average of 0.4%.

Rent Level Trends

The notion that homeownership is part of the American dream may not be for everyone. For many, it is a financial decision as well as one of convenience and flexibility. As a renter, you avoid many of the costs of homeownership that exceed the simple cost of a mortgage such as property taxes, homeowner’s insurance, HOA dues, routine maintenance and potential major repairs. If you have enough for a down payment but choose to rent, you can invest that down payment money in other assets that you feel may appreciate more than a home and avoid all that.

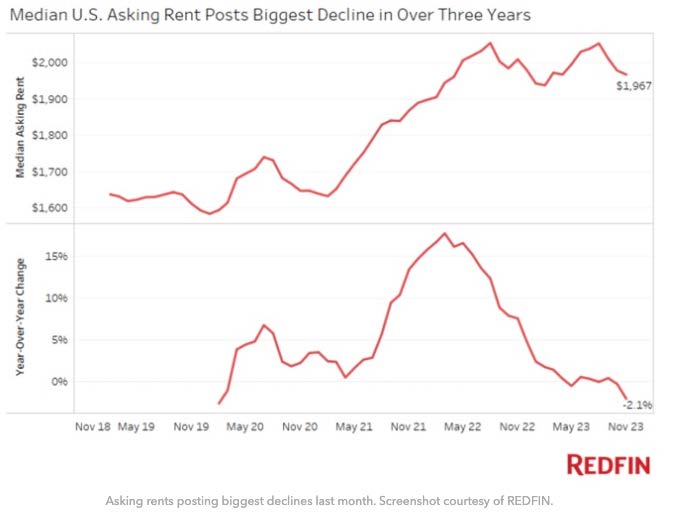

The charts below show nationwide rent trends in median asking rent amounts and the year over year change in those amounts. It’s clear that the pandemic surge in asking rent amounts came to a halt in 2023. Now we are starting to see declines in asking rent levels which will likely continue in 2024. That being the case, renting may be a better option if home values continue to rise and mortgage rates remain relatively high.

Wrapping Up

The impacts that the pandemic has had on the cost housing (ownership and renting), among many other aspects of traditional lifestyles, will be studied for years to come. I asked ChatGPT how much money the US government injected into the economy through pandemic related stimulus packages and all it says is “trillions”. Combine that with the Federal Reserve driving short term rates to near zero and there you have it. It’s hard to imagine that we will experience such a combination of factors again in our lifetimes. Only time will tell if we experience some reversal in home values over the next 5-10 years like we experienced during the 2007-2008 financial crisis.

To be sure, financial crisis was caused by structural issues within the banking sector, the aggressive use of adjustable-rate mortgages (ARMs), mortgage fraud and the enormous amount of leverage risk certain very large banks took on. Recall Michael Lewis’ book “The Big Short” (and movie) for a full explanation of what happened. Our banking system today is in much better shape, issuance of fixed rate loans far outweighs ARMs, credit quality has tightened up and the financial position of homeowners are stronger than they were back then. That all doesn’t mean home values will never go down again as I can assure you, they will. That we have apparently avoided a highly expected recession over the past 2 years, gives me reason to believe that values should remain fairly stable. When, not if, the next recession hits, home values will suffer but not enough in my view that would come close to reversing all the gains in housing over the past 3-4 years.