There are as many varied and opinionated 2024 outlooks as there are people and investment firms that publish them. If you just keep looking, you will eventually discover one that fits with what you are looking for. Taking a step back, it’s helpful to focus on key aspects of the financial markets instead of trying to sum it all up in a single opinion. The aspects I will focus on are:

- Inflation / Recession / Economic Growth

- Interest Rates & Fixed Income

- Equity Markets

Inflation / Recession / Economic Growth

One’s views on inflation go hand in hand with views on the potential for a recession. There are basically two camps in terms of the outlook: one camp that believes that we are in the midst of a soft landing now and the other camp that still believes the economy is heading into recession, albeit a mild one.

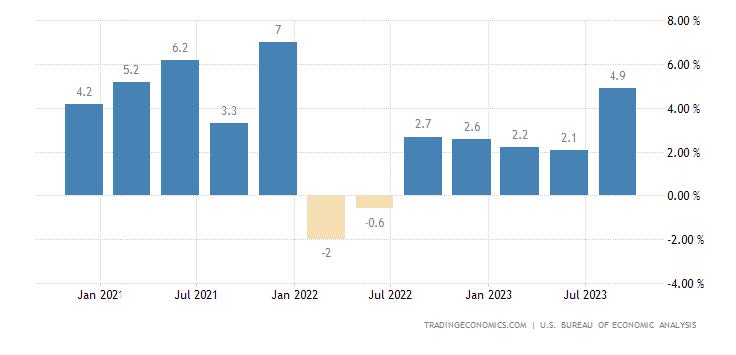

At the start of this year, there was broad consensus that our economy would slide into recession by the end of this year. Those views were misplaced since we are at year end and the economy grew at a robust 4.9% annual rate in the third quarter. Fears that the sharp rise in interest rates would hammer the economy were unfounded. That said, those who felt we would see a recession this year have not thrown in the towel. They feel high rates will eventually punish economic growth leading to a mild recession sometime in late 2024.

Also, inflation has dropped materially this year surprising many even though consumers may still be feeling the pinch of higher costs in many categories. The headline consumer price index (CPI) peaked at 9% in mid-2022 and as of November this year, it is only 3.1%. Throughout this period, unemployment has stayed below 4% for 22 months.

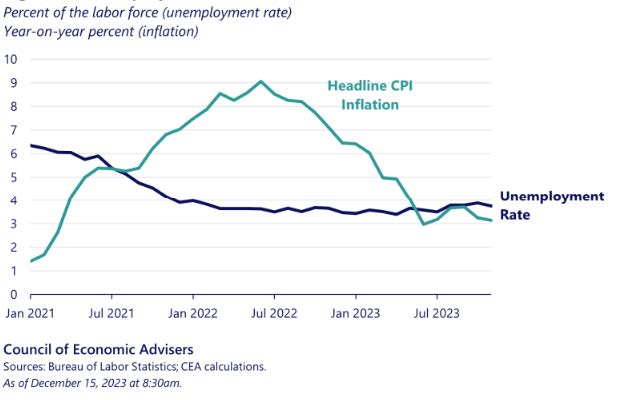

Unemployment and Inflation

It will likely be studied for years to come but the fact that the unemployment rate has held steady during this inflation cycle is remarkable. Taking folks back to your studies of economics, the often-cited Phillips Curve suggests that there is an inverse correlation between inflation and unemployment. As the chart below clearly shows, that is not always the case. The strength in the job market has surprised policy makers but is another indicator of the underlying strength in our economy.

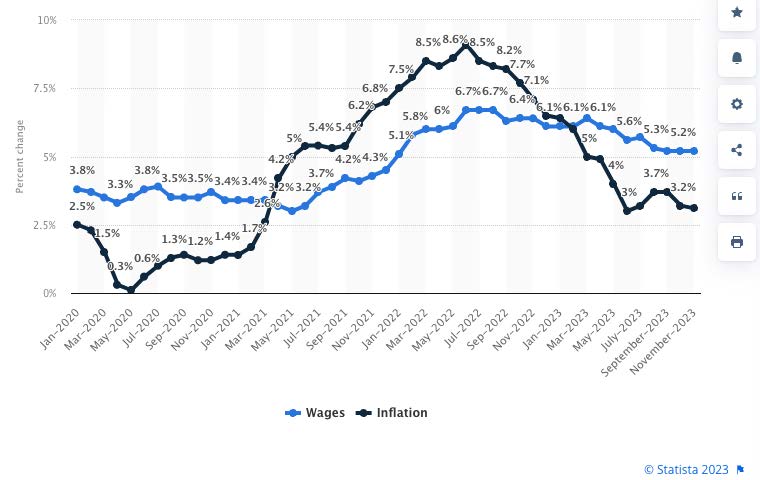

Wage Growth Exceeds Growth in Inflation

This is not necessarily what the Fed wants to see but the message appears to be that wage growth above the rate of inflation is good for consumers and is apparently not impacting inflation in a material way. The Fed watches wage growth closely because of the obvious link between higher wages leading to higher prices. At the moment, the Fed seems willing to accept the current situation given their pause in rate hikes at the most recent Federal Reserve Policy meeting.

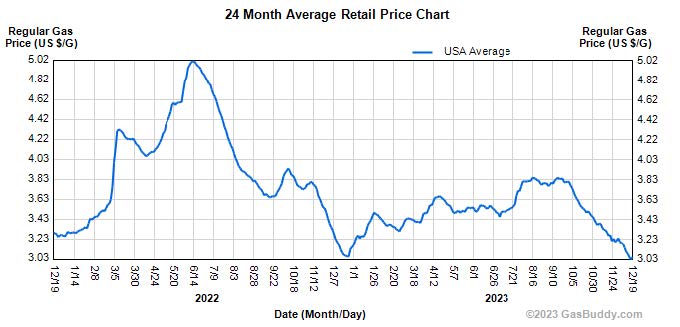

Not to be overlooked, the national average price of a gallon of gas has fallen from a peak of $5.02 in June of 2022 to $3.03. That alone is tantamount to a tax break for consumers that seems to be one of the reasons consumer spending has remained strong.

In the end, though, the Fed’s inflation target is 2% and it may take well into next year and maybe longer to achieve that goal.

Economic Growth

Given what the data above is showing, it’s interesting to me that there continues to be commentary out there that the economy is in bad shape. Summarizing some comments above:

- The job market has remained stronger than many expected given that in past rate cycles such as the one we are in have caused unemployment to noticeably rise.

- Wage growth also remains strong which is a key factor that the Fed watches in terms of when they may take their foot off the brakes.

- And inflation has dropped significantly.

Gross Domestic Product (GDP) has continued to grow throughout the year with the recent third quarter number a surprising +4.9%. Continued growth is projected for the fourth quarter which we won’t see until late January of next year.

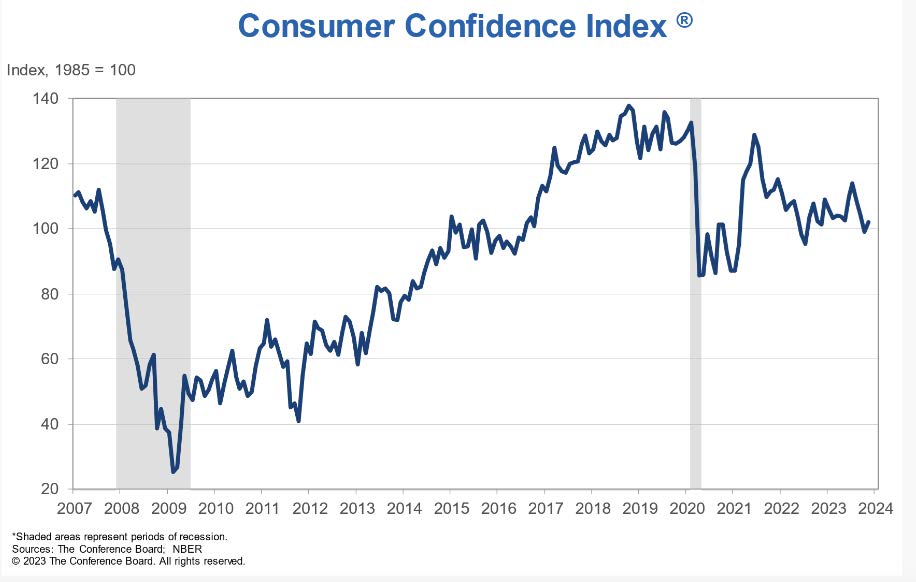

In addition, consumer confidence continues its slow climb from the sharp fall at the start of the pandemic.

Assessing all of the data above and more that I could highlight, I fall safely into the soft-landing camp because I feel the economy has weathered this rate hike cycle better than many seem to be acknowledging.

Interest Rates

I wrote about my interest rate outlook last month. Several key data points have yet to be published but my views haven’t changed.

- As I felt they would, the Fed left rates unchanged at their final meeting of the year. That wasn’t a tough call really as most everyone felt the same.

- The surprise was that Chairman Powell gave signals that there could be as many as 3 rate cuts of a ¼ point in 2024.

- As far as when the Fed may cut rates, I believe they will do so as early as May.

- There remains varied consensus on how low they push rates during 2024 but I feel a range between 4.00% and 4.50% (currently at 5.50%) is reasonable.

That said, 2024 should be a particularly good for bonds given the inverse correlation between bond values and interest rates. As market expectations of rate cuts in 2024 began to grow, interest rates began to fall fairly rapidly. Rates may stabilize over the coming months but the slow decline will likely continue well into 2024.

Equity Markets

An investment analyst at a major firm put together a short summary of 18 different investment firms’ 2024 outlook. The themes are fairly consistent and largely fall into the camp of slow earnings growth, no recession and lots of geopolitical risks. Common adjectives include: cautious outlook, moderate growth, concerns about global growth, etc.

As I mentioned at the beginning, if you keep looking, you can likely find an opinion out there that fits whatever opinion it is you are looking for. I don’t know how the markets will perform next year but I can say that there are several fundamental aspects discussed above that make me feel that 2024 will be a positive year for equities and bonds. International markets have been highlighted by many as having the potential of outperforming domestic markets which is normally not the case. Therefore, we are allocating higher than normal amounts to international markets in our models for clients. Adding in allocations to emerging markets, the total slightly exceeds our allocations to domestic markets.

Wrapping Up

Economics is not very exciting, I realize, but understanding what is actually happening leads me to be optimistic heading into 2024. A soft landing, falling interest rates, lower inflation, hourly wage gains, slow earnings growth, increased business and consumer confidence all point to a modestly positive environment next year. Market volatility has been quite low for several months now and could easily elevate in the new year. That’s just how markets react after a nice run up in prices. In other words, it will not be a straight line from here. As the year unfolds, we will always be reviewing our strategies to try and anticipate what the future holds and adjust accordingly.