Where to start? Here’s a quick summary of interest rates over the past two plus years.

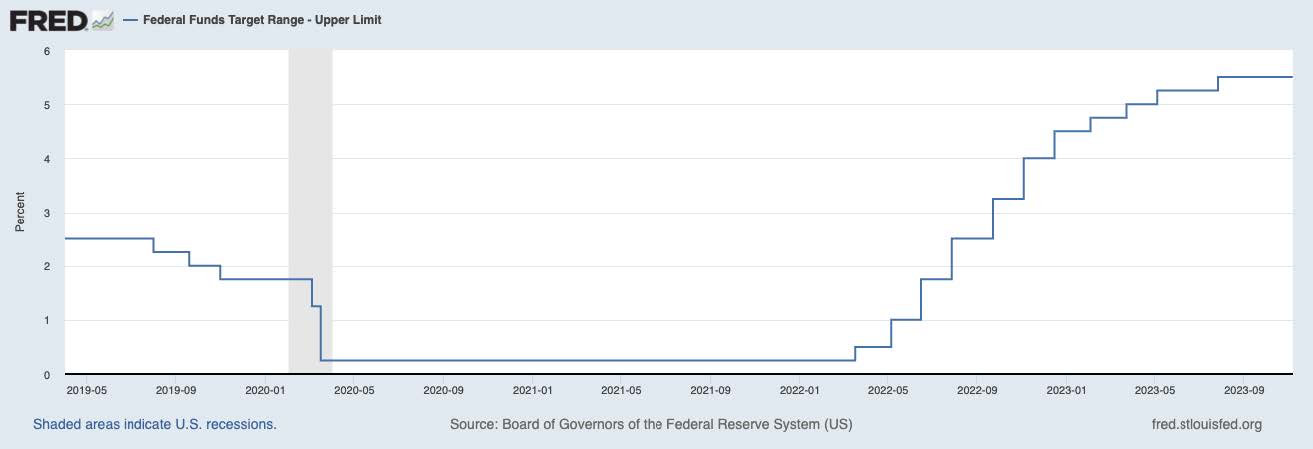

Leading up to the COVID pandemic, the Federal Reserve had embarked on a slow process of lowering the Fed Funds target rate from between 2% – 3% to 1% – 2%. When the pandemic went into full swing, they quickly took it to 0.25% and held it there until March 16, 2022 when they raised the target from 0.25% up to 0.50%. Since then, they have raised it 10 more times lifting it to a current 5.50%. Recall that the federal funds rate is the interest rate at which depository institutions trade federal funds (balances held at Federal Reserve Banks) with each other overnight.

It was the general consensus coming into 2023 that the rate hikes would lead to a recession by the end of this year which clearly hasn’t happened. That said, the Fed held rates steady at its most recent meeting last week due to a softening job market and the fact that mortgage rates have risen to a point such that the impact may help them achieve their goal of bringing inflation down closer to their 2% target rate. There are so many factors that go into trying to explain why interest rates fluctuate but suffice it to say that we are nearing the peak of the rise in the Fed Funds rate.

The questions everyone is trying to answer now; Is the Fed done raising rates? and When might the Fed start to cut the Fed Funds rate?

Is the Fed Done?

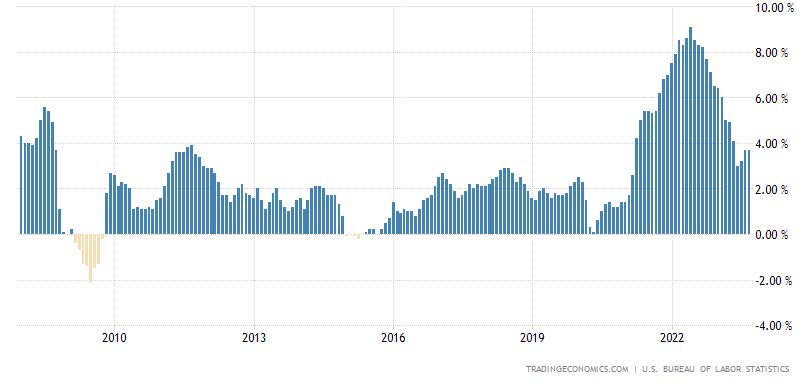

Last week Fed Chairman Powell danced around the question of more rate hikes in the future. He was careful not to commit to the notion they are done but the markets reacted in a way that seems to be anticipating that they are finished. As mentioned above, their target rate of inflation is 2%. The chart below tracks inflation going back to the financial crisis that began in 2008-2009. Since then, the rate has hovered roughly between 2% – 3% right up to the pandemic. The sharp rise from there was largely fueled by the trillions of dollars the Fed pumped into the economy to stave off a potential collapse in economic activity. No one expected that inflation would stay at rates in the 7% to 9% range long but getting back to 2% is not going to be easy.

We can talk about a lot of components in the CPI but the largest driver of inflation comes from the cost of Shelter. “Owner Equivalent Rent” (OER) data represents a 25% weighting of the value of the market basket of goods and services that comprise the Consumer Price Index (CPI). Add in “Rent of Primary Residence” (RPR) and you get to a total 33% weighting which is referred to as Shelter.

OER is essentially the equivalent rent that an owner would have to pay to live in a primary residence and is not based on the actual price of the property. It follows then that RPR, represents what a non-owner would pay in rent for a primary residence. With conventional mortgage rates in the 8% range, the cost of owning a home/apartment or renting the same, etc. remains very high. But given where we are now, inflation pressure from Shelter costs should moderate and help the Fed get closer to its inflation target.

If the rise in OER does moderate and other factors comprising the CPI begin to slow, it is easy to argue that the Fed’s job is done. Time will tell.

When Might the Fed Cut Rates?

This is a harder question to answer. Some, like the well-regarded Wharton Business School professor Jeremy Seigel, believe that the Federal Reserve needs to stay flexible and consider interest rate cuts a lot sooner than the market expects. At the time of this commentary, the Fed Funds futures pricing implies a roughly 85% probability that the Fed Funds rate will remain unchanged at 5.50% for the balance of this year. Futures pricing puts the total probability of rates being cut to 5.25% or below at the June 2024 FOMC meeting at 72%. By year end 2024, the futures are pricing in a probability of the Fed Funds rate being at 4.75% or lower. Seigel feels the Fed should cut rates by May of 2024 or sooner which the futures pricing is telling us has about a 50% chance. He argues that Chairman Powell runs the risk of being late to bring rates down just as he was roughly a year late to raise them as inflation was taking off. Futures pricing change rapidly and over the next several months of data, expectations could easily come more into line with his thinking or possibly cause folks to feel rates could stay “higher longer.”

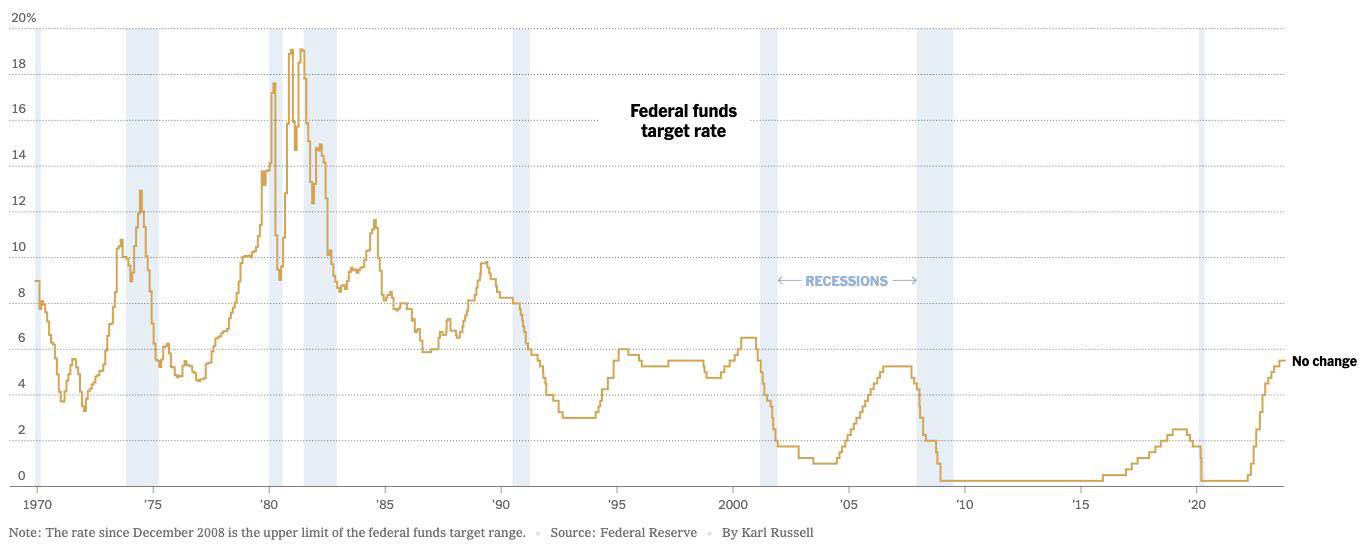

I added the chart below to give everyone a perspective for the volatile history of the Fed Funds target rate. The second chart mirrors the timeframe of the Fed Funds chart to show the high correlation of historical inflation rates and the Fed Funds target rates. It’s hard to imagine that the Fed Funds rate was as high 19% in the early 1980’s as we were coming off 15% inflation: the second highest inflation rate going back to 1970. You have to go back to roughly 1919 where the highest level reached just over 20% following the first World War.

Implications for Our Income Strategies

Given that the value of bonds decline as interest rates rise, 2023 has been a tough year for any bond holders. The longer the maturity of the bond instrument, the greater the price impact from rising rates. As the year unfolded, we began to focus on shorter maturity investments that gave us the flexibility to reinvest fixed income holdings at higher rates coming from the Fed tightening. For the past few months, we have begun to extend out the maturity of our fixed income holdings anticipating, as I discussed above, that we are at or very close to a peak in rates and that we will see rate cuts in 2024. That should bode well for our income strategies in that we can potentially recoup the some of the negative returns we have experienced this year.

Wrapping Up

The economy continues to surprise everyone by remaining more robust than anyone thought it would be this year. The Federal Reserve has struggled to get a handle on all the factors contributing to GDP growth, especially the very resilient job market and continued strong consumer spending. The softness in the most recent labor numbers was comforting to them but they are not fully convinced their job is done. The markets are betting that the Fed is done and that the Fed Funds rate will stay put for now. I see no reason to disagree with the sentiment on where rates will go from here. The lag between policy changes and the ultimate impacts are long and hard to predict so the Federal Reserve’s job is not an easy one by any means. For now, Chairman Powell seems willing to pause and see how this current lag time plays out before making his next move.