The supercharged pricing surges across much of our economy and the global economy are showing signs of abating. The news flow on reversing pricing trends is picking up so I thought it was time to take another look at where things are regarding price trends in important commodities and the supply chain situation. Should these lower price trends continue, we could see inflation pull back materially in 2023 as the pundits are beginning to predict.

As I write this, the June inflation report just released shows an annual increase in the consumer Price Index (CPI) of 9.1%, the largest 12-month increase since February 1981. Stripping out food and energy, the increase was 5.9%. Analysts forecasts for June CPI were 8.6% and 5.7% ex- food and energy. Mind you the reported numbers reflect historical price changes, not future prices. For example, the average price of a gallon of gas is now round $4.60, down from $5.00 a month ago which is not reflected in today’s report. Markets care about the future, not the past.

Industrial Commodities

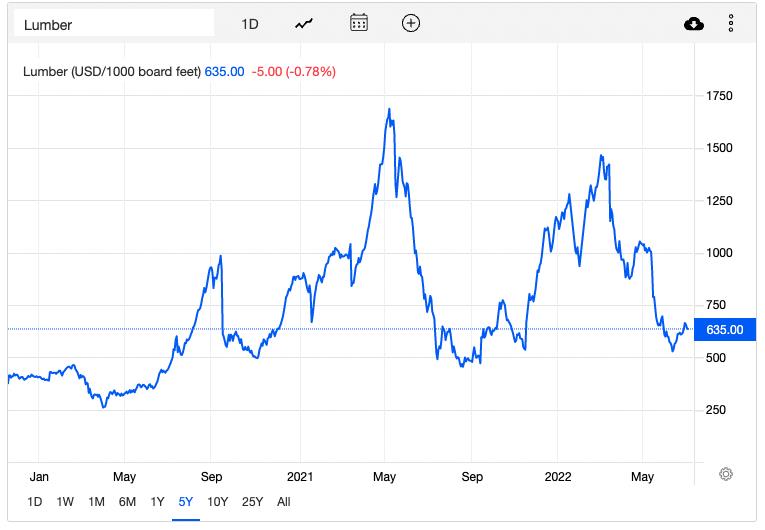

Looking at lumber pricing. I doubt it is news to anyone that lumber prices went near parabolic as the pandemic unfolded. Prices began soaring shortly after the pandemic hit the global economy in early 2020. The Random Lengths Framing Lumber Composite Price (FLCP), an industry benchmark, increased roughly 175 percent between April and September, setting all- time highs each of the final nine weeks over that span. In May 2021, the FLCP topped $1,500 per thousand board feet ($1,500/mbf)—nearly three times the pre-pandemic record. As of June 2022, the price has settled down in the low $600’s. Some believe prices will continue to decline down to pre-pandemic levels, but time will tell.

There is a lot of commentary out there for why pricing went so crazy. First, lumber mills were forced to close or reduce their production capacity as covid hit. Second, many people undertook DIY and renovation projects in 2020 because they were spending more time at home or now working from home. Inflation further affected the cost of lumber. I also read that as the production situation began to deteriorate due to covid, retail lumber yards began to over order (hoarding) supply. And of course, the supply chain situation made it worse.

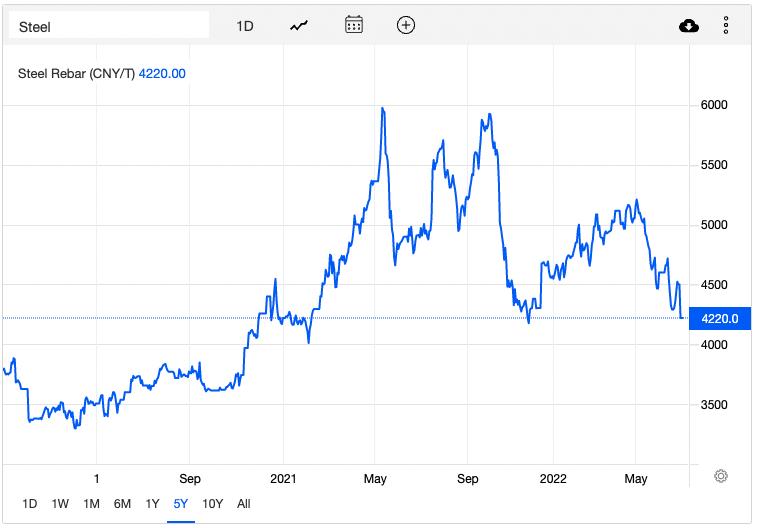

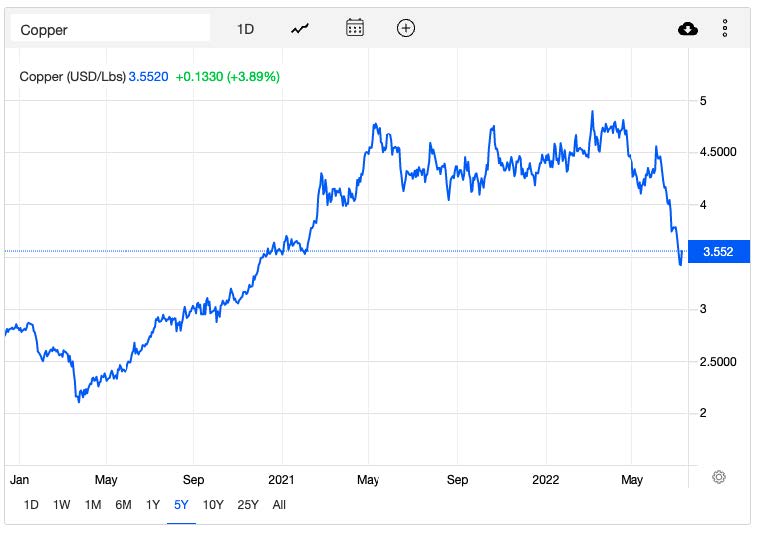

I believe the latest decline is due to rapidly rising interest rates and inflation that have cooled off the housing market. Again, something that is not lost on folks. More broadly, prices of additional industrial commodities such steel and copper are also softening and are largely correlated to lumber. See below for pricing trends on each.

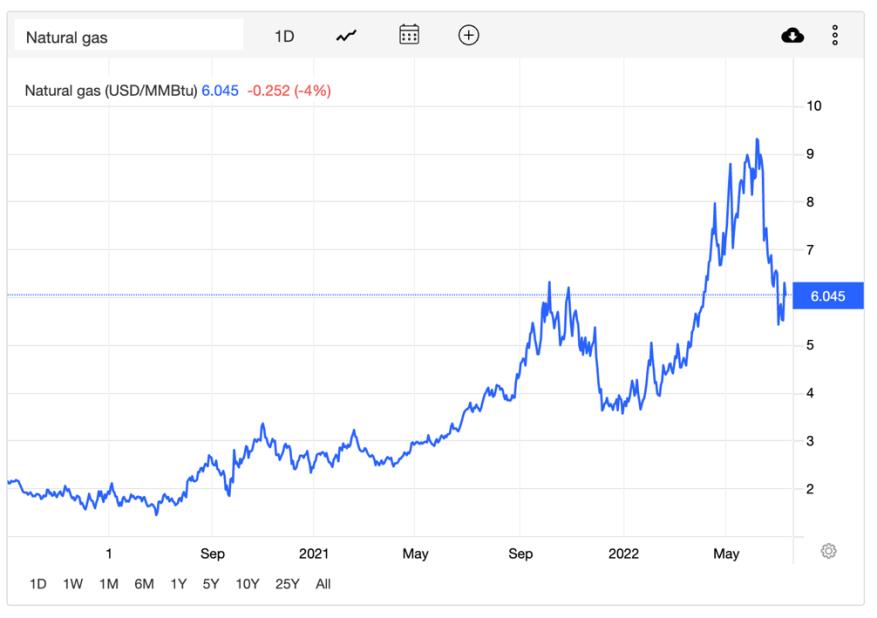

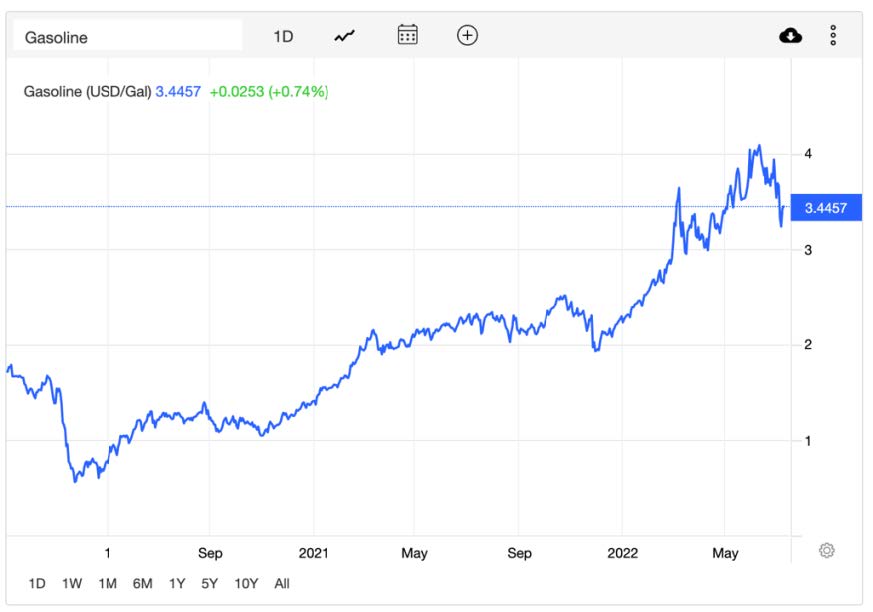

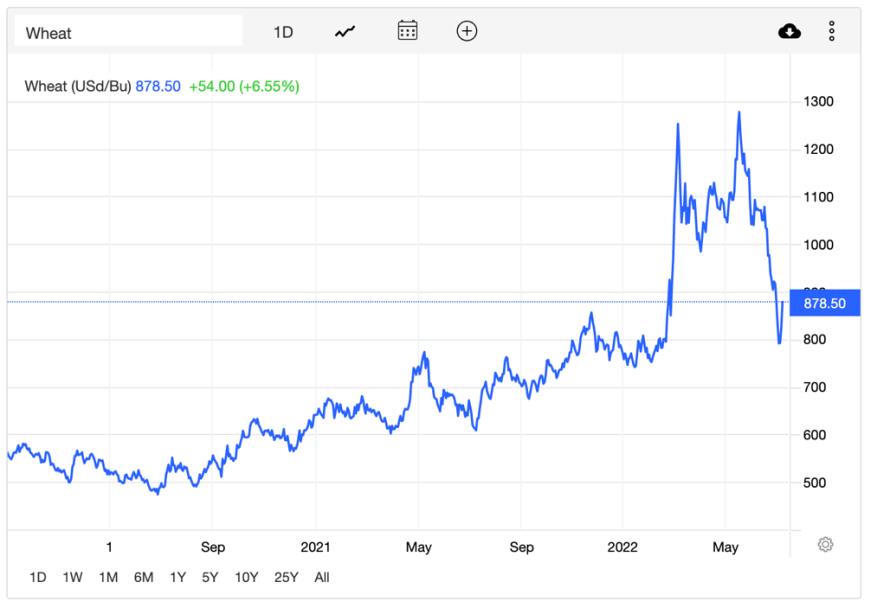

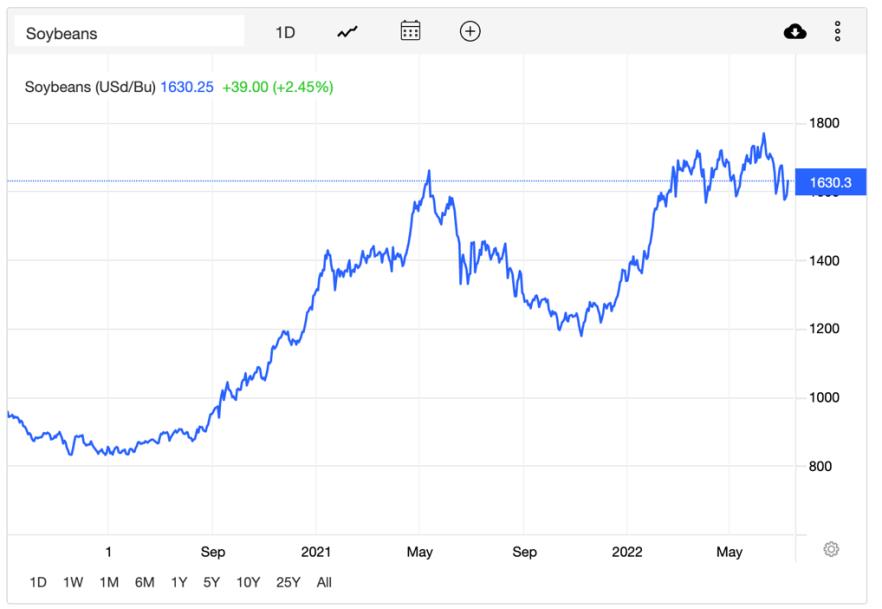

Natural Resource and Agricultural Commodities

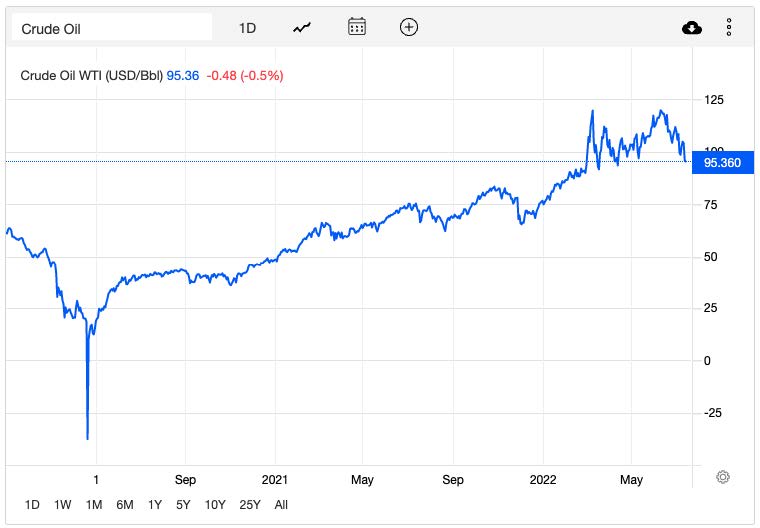

We have experienced sharply higher inflation during the last half of 2021 and into the first half of 2022, with rates exceeding 6.0% every month since October 2021. This is largely due to skyrocketing food and energy prices along with rising wage pressures. Various explanations can be given for these higher levels:

- Energy prices have increased, because of both governmental policies and the Ukraine- Russia war

- Food prices have increased because of strong global demand, supply chain issues and the Ukraine-Russia war

- Higher labor costs as employers raise wages to attract workers. Labor wage inflation that often translates into higher general inflation

But the outlook is slightly improving, for now. As recession fears grow so have price declines across most commodities due to expectation of lower demand. As we enter 2023, consensus is building that inflation will begin to cool off largely due to a pullback in elevated prices. To be sure though, wild price swings will likely continue due the global geopolitical and supply chain uncertainties. Below shows pricing trends for the futures on several important commodities. Futures are important in that they reflect expectations of what prices will be in the coming months.

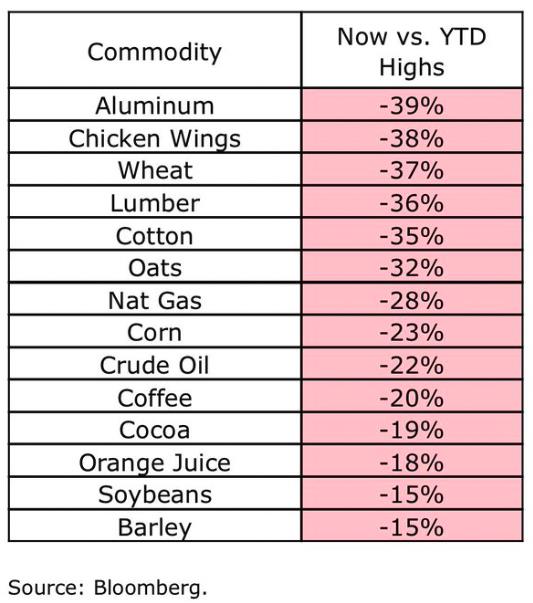

Here is a summary of price declines put together by Bloomberg. At some point, this will not be lost the markets.

Gold & Silver

Factors that impact the prices of gold are many:

- Gold’s Status as a Store of Value

- Gold’s Technological Use

- The Gold Supply

- Uncertainty About Gold

- Inflation and Gold

- Strength of the U.S. Dollar

- Interest Rates

- Government Actions – Central Banks

- The Jewelry Industry

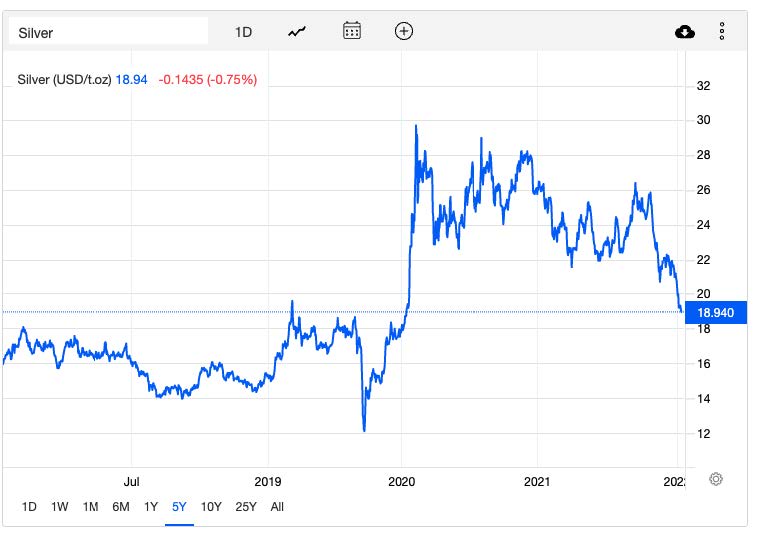

Silver prices are impacted by many of the same factors but given the greater abundance of the metal and its greater use in industrial applications, prices are much more volatile. The 5-year price graphs of each metal below illustrate the difference in price action.

In March 2020, both metals saw a quick drop in price closely followed by sharp rallies. Lower interest rates, a weak dollar related to massive stimulus and economic concerns were the primary factors for the rallies. Silver prices surged far more than gold and as you can see. Gold prices have held up better since early 2020, largely due investors’ preference for gold as a store of value over silver. A slowing economy has also negatively impacted silver prices more than gold.

Dollar strength continues to weigh of prices of both metals since they are both metals closely track the dollar. That results in lower foreign demand given that foreign currencies lose purchasing power as the dollar value rises. Going forward, my view is that gold will continue to be favored over silver but expect greater than average volatility for to continue for some time.

Supply Chain Constraints

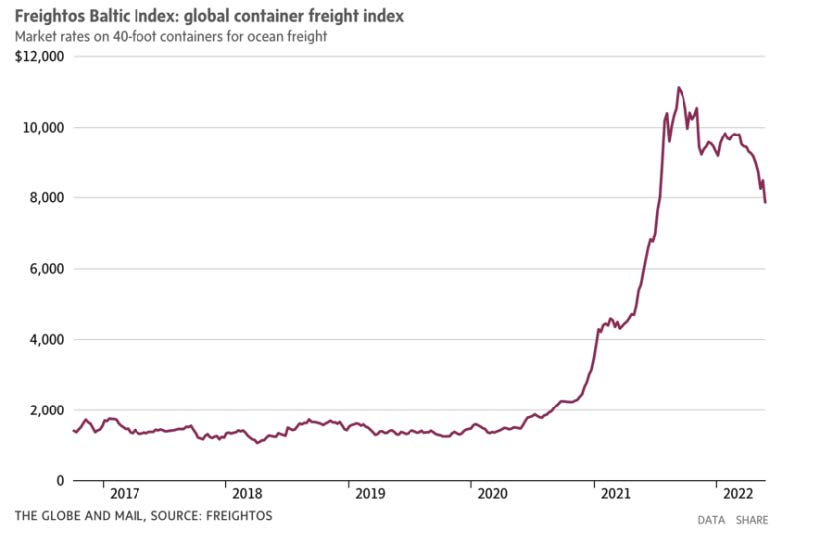

The current state of the supply chain remains quite a mess but is improving. One of the best indicators to reflect trends in the supply chain is the cost of a container to service various active trade routes globally.

Costs for shipping goods in containers have been dropping since March of this year, though experts say it’s too early for retailers to celebrate as congestion in the global supply chain lingers and consumer spending shifts. During most of the past two years, the costs for

transporting shipping containers ballooned as people altered their purchasing behavior to favor physical goods. Now, consumers are increasingly spending their disposable income on services rather than household items and reacting to climbing interest rates.

The gradual improvement in moving shipping container out of ports and to distribution centers has led to a glut of inventory at retailers. Products such as consumer electronics, sporting goods, apparel and accessories are piling up and store shelves are full. Estimates are that some stores are more 30% overstocked. This is leading to what is being described as “Retail

Armageddon” as deep discounts show up in stores across the country. The graph below shows just how rapidly the cost of a container has risen since the beginning of the pandemic. The recent weakness is due to reduced demand related to the Russian/Ukraine war freeing up supplying of containers. Container costs are anticipated to continue declining but will stay well above pre-pandemic levels for the foreseeable future.

Wrapping Up

My goal in this commentary is to make the point that disruptions from covid and related impacts to economies globally are slowly beginning to diminish.

Economists and the Federal Reserve completely blew it last year by sticking with the belief that inflation pressures would be transient. Now the hapless Federal Reserve is running the risk of pushing too hard on the brakes indicating several more aggressive fed funds rate hikes by year end.

The greater than expected June inflation report almost guarantees the Federal Reserve will hike the Fed Funds rate by 75 basis points at the July 27th meeting.

The risks of pricing trends reversing higher are real and can happen quickly as we saw when Shanghai went abruptly into full covid lockdown mode recently due to their zero-tolerance policy. It just demonstrates how fragile economic activity is now.

The markets are going to remain volatile for some time as analysts and traders try to anticipate short term indicators without much focus on the long term which is what we need to be doing. These are unique times, so I encourage you to reach out at any time to talk about trends and how we are positioning portfolios to weather the storms.