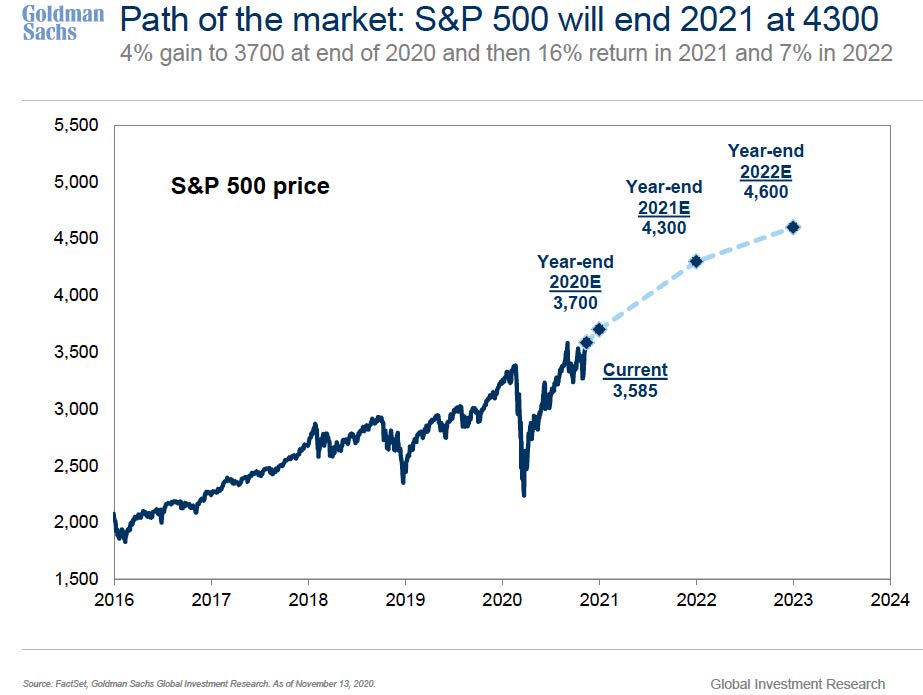

A year to put behind us. The combination of the COVID-19 out break and a hotly contested election cycle made for enormous amounts of uncertainty, the likes of which we haven’t experienced for many, many years. There will be lasting impacts from both of these events that will be felt for years to come. That said, I feel that the year ahead will present a more predictable political environment and a reversion to the mean in terms of stock market performance. When one party is in the White House and another holds the Senate, gridlock is predictable, and markets tend to like predictability. Even so, I don’t believe we are completely out of the woods when it comes to market volatility. In fact, I fully expect us to experience volatility that could potentially result in a 10% correction or more at some point during the year. In general, though, I do feel the worst of it is behind us, at least for the time being. Surveying the spectrum of market forecasts, the general consensus lays out year-end 2021 projections of gains between 8-12% in the major stock indices from today’s levels.

COVID-19

The massive rollout of currently approved vaccines is underway with hopes that by summer, life could begin to return to some semblance of normal. Between now and then, though, the sharp rise in confirmed cases may continue into the early spring with projections of peaking in March. It is unclear to me if investors are expecting the peak in confirmed cases to occur sooner than that. If so, we could experience some volatility as we head into the spring. Either way, I do believe that as the rollout progresses, tensions around all the mask requirements and stay at home orders should begin to settle down which should support a path back to economic growth.

Economic Trends

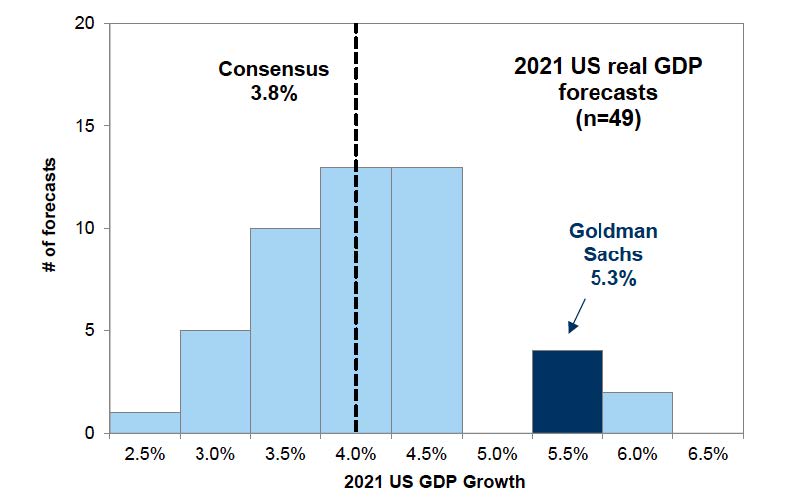

After a whipsaw year of GDP performance this year, most economists are looking for 2021 normalized growth in the range of 3.5% to as high as 6% with consensus being 3.8%. What is missing from the Goldman Sachs chart below is the fact that almost all growth in 2021 will come in the second half of the year due to expectations that the world will begin the return to normal economic activity.

I believe as 2021 unfolds, the markets will focus on second half 2021 outlooks and start looking at prospects for economic growth in 2022. Economic trends for 2022 will not start taking shape until mid-year, so until then we remain hopeful that the path out of the COVID economic slowdown will become clearer.

Inflation

Inflation expectations are going to have an important role in how interest rates move over the next 12-18 months. I wish I could say there is a consensus among all the estimates of inflation changes over that time frame. On one end of the spectrum, Albert Edwards, the global economist for Société Générale, a well-known global investment bank, believes that we are heading into an era where inflation could go to zero once the sharp decline in rents begins to put pressure on GDP growth. Changes in rental prices take a long time to filter through to CPI but they make up nearly 40% of CPI calculations. He feels others are too sanguine on that point. Declining rents can lead to lower economic growth hence lower profit growth which of course is not good for markets.

At the other end of the spectrum, with which I am more in agreement, is the expectation that inflation rates will rise for the simple reason that the US government has pumped more than $3T into the economy this year with $900B just approved coming by Christmas. With today’s news of Trump now asking for $2,000 checks vs $600 which is in the bill, the entire effort is at risk of dragging into the new year. Odds of that outcome are low in my view and that something will get done over the next few days. The incoming administration has also already made it clear that even more stimulus will be coming in the first half of the year as the ongoing spike in infection rates continues. I believe the decline in rents will stabilize in 2021 as the economy gradually gets back on track. I have spoken with many of you about the broad implications of skyrocketing government debt levels but suffice to say that in my view the odds of inflation rising over the next couple of years outweigh odds of declining. Below are inflation estimates from the Federal Reserve which reflect modest inflation in contrast to Edward’s outlook.

Core PCE Inflation – Federal Reserve Estimates

To be sure, higher inflation is not necessarily a bad thing. Real estate, in particular rental properties, can benefit as rising mortgage rates make renting cheaper than buying. We often talk about owning real estate and I know that some of you own or have owned rental properties. Many of you know that we have always been fans of having real estate as part of a long-term financial plan.

Wrapping up 2020

It would be irresponsible to not reflect on how certain parts of the equity market are at or exceed valuations we haven’t seen since the Dot-Com bubble of 2000-2001. Megacap technology and communication companies (many of which have yet to report a profit – Unicorns in Wall Street speak) have led the markets higher while the broader market has generally been pretty quiet. We here at MCIA have often discussed these trends and have been in close contact with the fund managers we incorporate into our investment strategies. Many of you have heard us discuss the performance of growth vs value and how we firmly believe that we are entering a period of slow transition from a focus on growth to a focus on value. It is not an abrupt change in portfolio strategies but one that will occur in the coming quarters as opportunities to shift capital appear. We will be continually communicating these changes and rationale as they occur in the new year.

As the year comes to a close, I along with the entire MCIA team want to thank you for your confidence and support as we exit 2020. We all wish you the happiest of holidays and a safe New Year!!